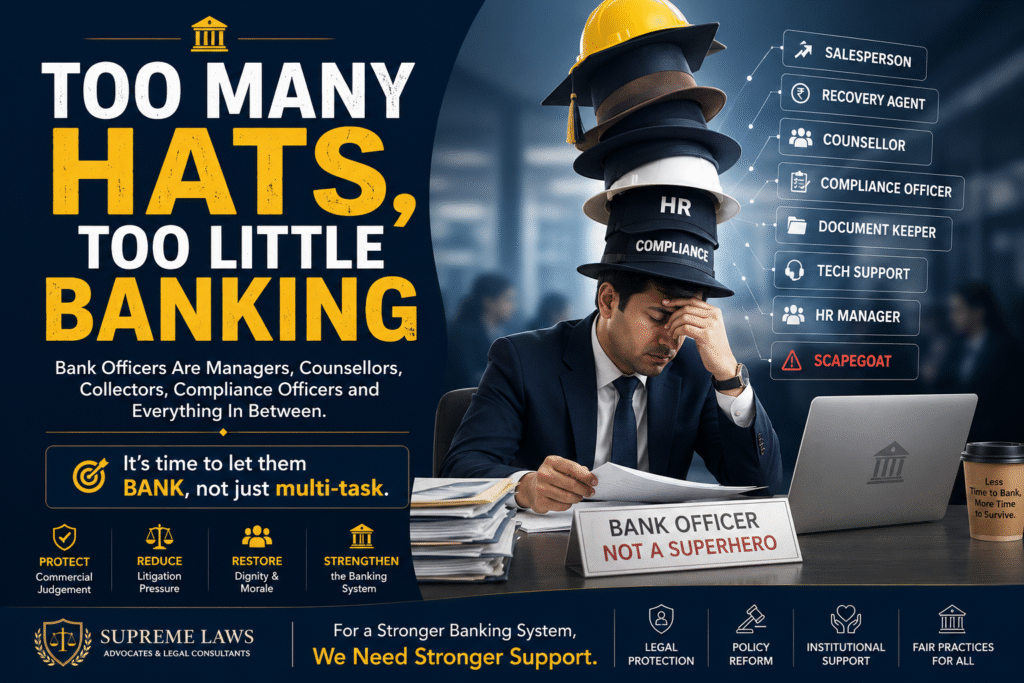

India’s banking sector has become the backbone of economic growth, yet its efficiency is increasingly undermined by the growing burden of non-banking responsibilities placed on bankers. Besides mobilizing deposits, assessing creditworthiness, and managing financial risks, they are expected to undertake gold evaluation, property and land assessment, title verification, machinery valuation, insurance coordination, legal compliance, recovery proceedings, and extensive documentation. Many of these technical assignments should be handled by qualified valuers, engineers, and legal experts. Diverting bankers from their core responsibilities results in slower customer service, delayed loan sanctions, reduced branch efficiency, mounting workplace stress, declining productivity, and higher operational risks.

The consequences of this misplaced allocation of work are evident across the banking system. Bank employees are often held accountable for technical decisions beyond their professional expertise, such as gold valuation, land assessment, construction inspection, or market valuation. These tasks require specialized knowledge and independent professional judgment. Performing them increases the risk of inaccurate valuations, fraud, legal disputes, and financial losses. Simultaneously, business targets and regulatory obligations create additional pressure, reducing productivity and customer confidence. Instead of concentrating on prudent lending and relationship management, bankers become multitasking administrators performing duties that specialized professionals could handle more effectively.

A practical solution lies in redefining the operational framework through policy intervention by the Government of India, the Reserve Bank of India, and banking regulators. A nationwide network of accredited professionals should undertake specialized functions such as gold valuation, property assessment, engineering inspections, and legal due diligence. Banks should rely exclusively on certified valuers, engineers, surveyors, and legal experts operating under statutory accountability. Digital platforms can streamline report submission and verification, while periodic audits, performance ratings, and strict penalties ensure transparency. This specialization would reduce operational risks and enable bankers to focus on credit analysis, customer service, fraud prevention, and portfolio management.

The successful implementation of these reforms requires a phased and coordinated policy approach. The Ministry of Finance, RBI, Indian Banks’ Association, and banks should jointly issue uniform operational guidelines clearly defining the responsibilities of bankers and external experts. Banking manuals should prohibit branch officials from independently conducting technical evaluations where certified professionals are available. Pilot projects can refine procedures before nationwide implementation, supported by digital integration with accredited service providers. Regular monitoring through indicators such as processing time, credit quality, customer satisfaction, and employee productivity will ensure measurable success. Allowing bankers to focus exclusively on banking will strengthen operational efficiency, improve lending quality, reduce avoidable risks, and support sustainable economic growth.